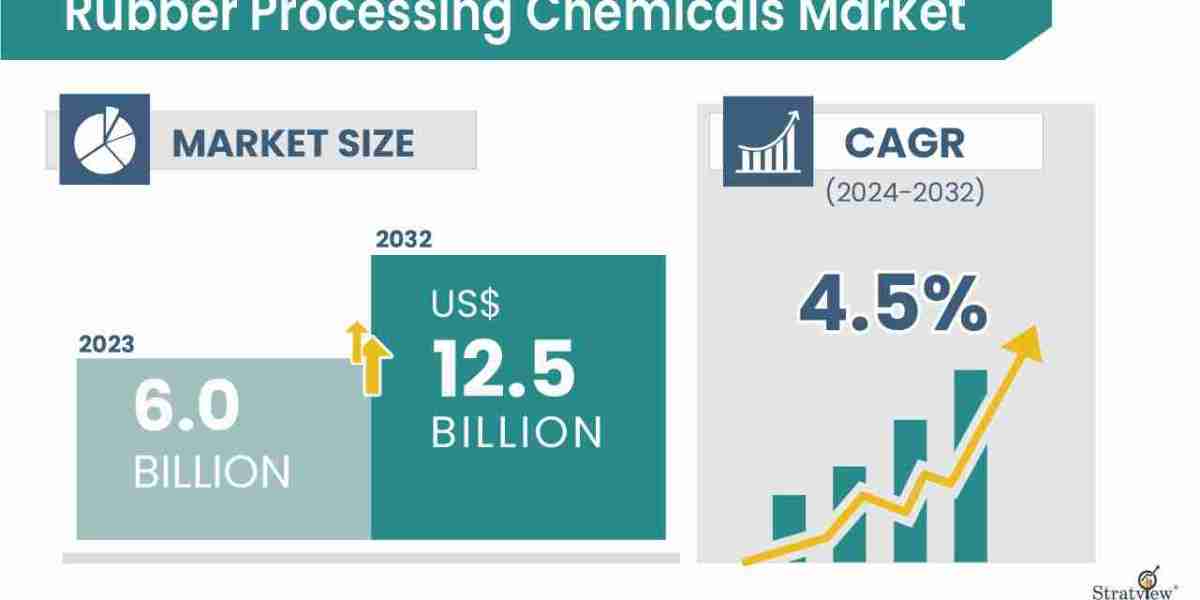

The Rubber Processing Chemicals Market was valued at USD 6.0 billion in 2023 and is expected to reach USD 12.5 billion by 2032. The market is projected to grow at a CAGR of 4.5% during 2024-2032, supported by demand from tire manufacturing, automotive production, and industrial rubber applications.

The Rubber Processing Chemicals Market Forecast points to steady expansion, supported by tire manufacturing, industrialization, and the growing need for rubber products with better durability. Asia-Pacific remains central to future demand because of its strong automotive production base, major tire manufacturers, and expanding industrial rubber consumption across China, India, and Japan.

Rubber processing chemicals improve the physical and mechanical properties of rubber products. These additives help rubber withstand environmental conditions and support smoother production. Common chemicals include accelerators, anti-degradants, processing aids, and curing agents.

Request a free sample report: https://www.stratviewresearch.com/Request-Sample/4452/rubber-processing-chemicals-market.html#form

The key growth driver is the automotive sector, especially tire manufacturing. Tires require chemicals that improve durability, resistance to wear and tear, and performance across terrain conditions. As automotive production rises, demand for specialized rubber chemicals increases structurally.

Market Segmentation Analysis

By Product Type

Anti-degradants (Regional Analysis: North America, Europe, Asia-Pacific, and RoW)

Accelerators (Regional Analysis: North America, Europe, Asia-Pacific, and RoW)

Flame Retardants (Regional Analysis: North America, Europe, Asia-Pacific, and RoW)

Processing Aid/ Promoters (Regional Analysis: North America, Europe, Asia-Pacific, and RoW)

Others (Regional Analysis: North America, Europe, Asia-Pacific, and RoW)

By Application Type

Tire (Regional Analysis: North America, Europe, Asia-Pacific, and RoW)

Non-Tire (Regional Analysis: North America, Europe, Asia-Pacific, and RoW)

By Region

North America (Country Analysis: The USA, Canada, and Mexico)

Europe (Country Analysis: Germany, France, The UK, Russia, and Rest of Europe)

Asia-Pacific (Country Analysis: Japan, China, India, and Rest of Asia-Pacific)

Rest of the World (Country Analysis: Brazil, Saudi Arabia, and Others)

The anti-degradants segment led the market, accounting for 50% of the total share in 2023. Anti-degradants protect rubber from degradation caused by oxygen, ozone, heat, UV radiation, and oxidation. This extends product life, making the segment strategically important for manufacturers focused on durability.

The tire application represents the largest share of the market. Tire manufacturing is the biggest consumer of rubber processing chemicals, as tires need additives for durability, resistance to environmental degradation, and mechanical stress performance. This links automotive production directly with demand for rubber chemical formulations.

Explore the latest market analysis and forecasts for the Rubber Processing Chemicals Market: https://www.stratviewresearch.com/4452/rubber-processing-chemicals-market.html

The non-tire segment is included in the application structure, but the source does not state its dominance or fastest-growing status. Its strategic relevance comes from the broader use of rubber products across industrial and consumer goods applications, where performance consistency remains important.

Regional Market Insights

Asia-Pacific is the largest and fastest-growing market for rubber processing chemicals. The region’s demand is driven by high automotive production and industrial growth in China, India, and Japan. The presence of large tire manufacturers further increases chemical consumption across rubber production.

Asia-Pacific’s growth is structurally tied to its automotive manufacturing base. Since the automotive sector is the largest consumer of rubber processing chemicals, especially for tire production, high vehicle output creates sustained demand for additives that support durability and performance.

Emerging Trends Shaping the Rubber Processing Chemicals Market

The Rubber Processing Chemicals Market is being shaped by performance needs in tire and industrial rubber products. Anti-degradants remain central because they protect rubber from environmental stressors and extend product lifespan.

A clear industry direction is the development of low-VOC and eco-friendly rubber additives. Lanxess launched low-VOC rubber additives in 2023, while Eastman Chemical Company entered a joint venture focused on sustainable rubber processing chemicals.

This direction reflects rising regulatory demands for eco-friendly chemicals. As manufacturers work to improve environmental performance, product development and industry partnerships are becoming important parts of the market outlook.

Key Growth Drivers of the Market

- Automotive production increases tire demand, and tires require anti-degradants, accelerators, and vulcanization agents to improve durability, resistance, and performance.

- OEM demand for high-quality tires raises the need for specialized rubber processing chemicals that support wear resistance and mechanical stress performance.

- Infrastructure expansion and industrialization increase the need for advanced rubber products, which raises demand for chemicals that improve strength and durability.

- Regulations for eco-friendly chemicals are encouraging sustainable rubber processing chemicals, creating demand for lower-emission and environmentally focused additives.

- A fragmented industry ecosystem with over 500 players intensifies competition around price, service offerings, and regional presence, strengthening product range development.

Competitive Landscape

Top Companies in the Market

Akzo Nobel N.V.

Arkema

BASF SE

Behn Meyer

Eastman Chemical Company

KUMHO PETROCHEMICAL

Lanxess

Paul & Company

R.T. Vanderbilt Holding Company, Inc.

Solvay

The market is highly fragmented, with the presence of over 500 players across the region. Major players compete on factors including price, service offerings, and regional presence. Some leading companies provide a complete range of rubber processing chemicals.

Conclusion and Strategic Outlook

The Rubber Processing Chemicals Market is expected to grow from USD 6.0 billion in 2023 to USD 12.5 billion by 2032. The market forecast reflects a CAGR of 4.5% during 2024-2032.

The growth trajectory is supported by tire manufacturing, automotive production, industrial rubber demand, and the use of additives that improve rubber durability. Anti-degradants remain the leading product type, while tire remains the largest application.

Asia-Pacific is both the largest and fastest-growing region. Its strong automotive manufacturing base, large tire manufacturers, and industrial growth make it central to the market’s long-term demand structure.

FAQs – Rubber Processing Chemicals Market

What is the market size and forecast for the Rubber Processing Chemicals Market?

The Rubber Processing Chemicals Market was valued at USD 6.0 billion in 2023. It is expected to reach USD 12.5 billion by 2032, growing at a CAGR of 4.5% during 2024-2032.

What are the major growth drivers of the market?

The key drivers include demand from the automotive industry, especially tire manufacturing. Industrialization, infrastructure development, and demand for durable rubber products also support market growth.

Which region leads the rubber processing chemicals market?

Asia-Pacific leads the global market and is also the fastest-growing region. Its growth is driven by high automotive production, industrial growth, and strong demand from China, India, and Japan.

What is the investment outlook for the market?

The market outlook is supported by a forecast value of USD 12.5 billion by 2032 and steady growth during 2024-2032. The presence of over 500 players indicates a fragmented and competitive market structure.

What risks or constraints should companies consider?

Companies should consider competition based on price, service offerings, and regional presence. Rising regulatory demands for eco-friendly chemicals may also influence product development priorities and manufacturing choices.