Global Automotive Front-End Module Market Engineered for Disruptive Transformation: Projected to Surpass USD 166.07 Billion by 2030, Catalyzed by EV Integration and Composite Materialization

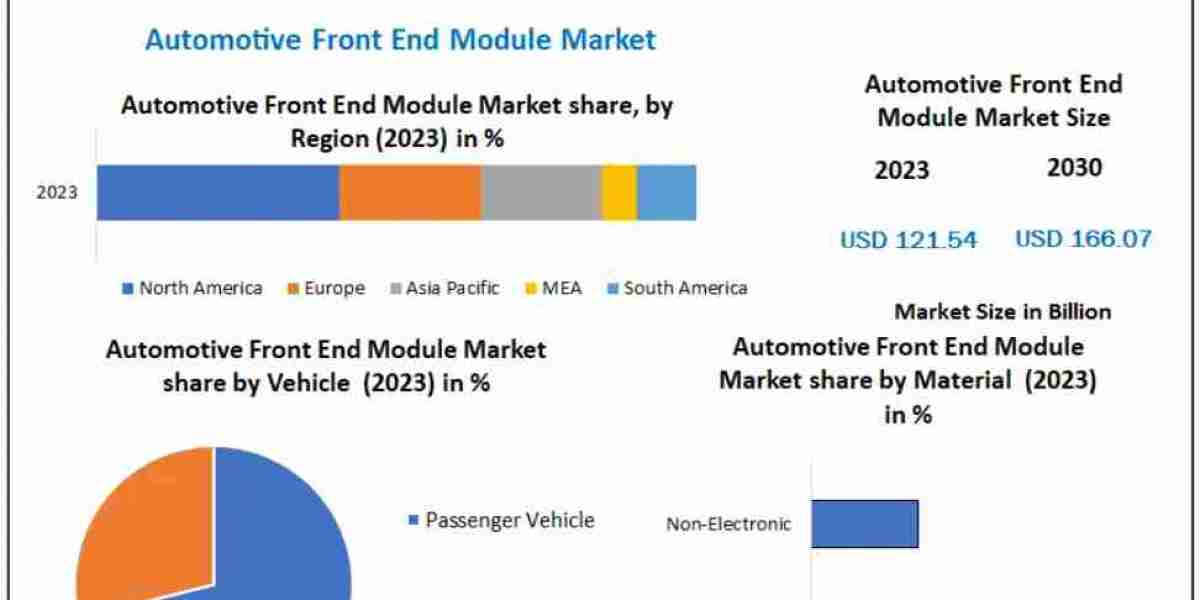

Valued at an impressive USD 121.54 Billion in 2023, the global Automotive Front-End Module (FEM) Market is systematically executing a major structural and material revolution. According to a comprehensive intelligence study released by Maximize Market Research, the market is projected to expand at a steady Compound Annual Growth Rate (CAGR) of 4.56% over the forecast period, ultimately reaching an estimated valuation of USD 166.07 Billion by 2030.

This sustained upward trajectory is underpinned by a profound paradigm shift within global automotive manufacturing. Original Equipment Manufacturers (OEMs) are actively moving away from traditional fragmented vehicle assembly processes in favor of highly integrated, pre-assembled multi-piece structural systems. Driven by intense regulatory compliance demands, escalating global electric vehicle (EV) penetration, and a critical requirement for vehicle weight reduction, the automotive front-end module has transformed from a simple structural bracket into a complex, high-technology system core.

???????? ???? ??? ???????? @https://www.maximizemarketresearch.com/request-sample/16726/

Understanding the Automotive Front-End Module: The Hub of Next-Generation Vehicle Architecture

An Automotive Front-End Module (FEM) is a comprehensive, multi-piece structural assembly located at the absolute fore of a vehicle. Rather than forcing assembly lines to mount dozens of separate brackets, components, and fasteners individually, modern automotive engineering utilizes the FEM as a unified structural carrier. This carrier integrates a dense network of critical functional subsystems, including:

Forward Lighting Systems: Advanced LED, matrix, and laser headlamp assemblies, along with integrated leveling sensors.

Thermal Management Elements: High-efficiency radiators, electric cooling fans, oil coolers, and Air Conditioning (A/C) condensers.

Structural Reinforcements: Grille-Opening Reinforcement (GOR) panels, energy-absorbing bumper assemblies, and integrated crumple zones engineered for crashworthiness.

Aerodynamic Components: Active grille shutters, air ducts, and aerodynamic belly pans designed to lower the vehicle's drag coefficient.

Electronic Control Networks: Advanced Driver Assistance Systems (ADAS) sensors, radar units, cameras, ambient temperature sensors, hood latches, and complex wire harnessing.

By consolidating these disparate parts into a single structural module, tier-1 suppliers and OEMs can streamline their assembly floors. This architectural approach not only simplifies the physical footprint of the vehicle assembly line but also dramatically improves dimensional accuracy and consistency, lowering the probability of geometric misalignments across vehicle platforms.

Accelerated Market Dynamics: The Intersection of EV Proliferation and Lightweighting

The global automotive sector is undergoing its most significant structural shift in a century, driven by the rapid transition toward electrification. The surge in global electric vehicle sales—which continue to seize an expanding share of the global passenger car market—acts as a primary catalyst for the specialized automotive front-end module market.

Traditional front-end designs were heavily optimized around internal combustion engines (ICE), focusing primary layout attention on heavy mechanical ventilation and engine block clearance. In stark contrast, electric vehicles present entirely distinct architectural requirements. Front-end modules developed explicitly for EVs must accommodate:

Specialized Battery and Powertrain Cooling: While EVs eliminate the traditional engine radiator, they introduce sophisticated, multi-circuit thermal management systems required to maintain optimal battery pack, inverter, and electric motor temperatures.

Advanced Aerodynamic Integration: Because electric vehicle driving range is heavily dictated by aerodynamic drag, modern EV front-end modules are intricately sculpted to optimize airflow, integrating hidden active air flaps that open only when thermal cooling is strictly required.

Sensor Enclosures for Autonomous Driving: The front-end module serves as the primary mounting face for autonomous and semi-autonomous driving suites. Radar, LiDAR, and ultrasonic sensors must be seamlessly embedded into the FEM carrier with precise calibration to ensure reliable safety tracking.

To counteract the substantial weight of large lithium-ion battery packs and maximize driving range, the automotive industry has placed an unprecedented premium on lightweighting. Every single kilogram extracted from the vehicle structure directly translates into extended battery efficiency. Consequently, the demand for pre-assembled, structurally optimized front-end modules constructed from advanced lightweight materials has reached an all-time high.

Production Line Economics: Reducing OEM Assembly Costs by 20% to 30%

Beyond the technical benefits to the vehicle itself, the adoption of modular front-ends delivers immediate financial advantages to manufacturing operations. The integration of automotive front-end modules is fundamentally revolutionizing modern passenger vehicle assembly plants by shifting labor-intensive, multi-component sub-assembly processes away from the main assembly floor and into highly optimized tier-1 supplier facilities.

Industry data confirms that implementing pre-assembled modular front-ends can reduce direct vehicle assembly line production costs by approximately 20% to 30%. This significant financial saving is achieved through several operational improvements:

Streamlined Logistics: Instead of managing inventory, quality control, and supply chains for over 40 individual front-end parts, an OEM receives a single, fully tested, plug-and-play assembly unit at the assembly bay.

Enhanced Assembly Ergonomics: Workers or robotic arms can bolt the entire front-end module onto the main body chassis in a fraction of the time, allowing for wide-open access during engine, motor, and major suspension system installations.

Platform Standardization and Scalability: Global vehicle manufacturers can utilize a standardized front-end module structural core across multiple distinct vehicle models or global platforms, allowing for exterior styling differentiation via customizable plastic fascia while keeping internal architecture uniform.

Material Science Breakdown: The Evolution from Steel to Composites

The historical trajectory of front-end carrier design highlights a steady shift away from traditional, heavy all-metal architectures toward highly sophisticated material combinations. Over the past decade, material science has completely transformed the weight-to-stiffness ratio of vehicle structures.

As highlighted by these historical milestones, the market is actively prioritizing the Composites segment. Long glass-reinforced thermoplastics, processed via advanced direct long-fiber thermoplastic (D-LFT) methods, are rapidly gaining market share. These materials offer high mechanical strength, excellent corrosion resistance, high design freedom, and the unique ability to mold complex fastening tabs and air ducts directly into the main structure, entirely eliminating secondary joining operations.

???????? ???? ??? ???????? @https://www.maximizemarketresearch.com/request-sample/16726/

Detailed Market Segmentation Analysis

To provide a clear vision of the industry's direction, the global Automotive Front-End Module Market can be analyzed across several key segments: Vehicle Type, Material Composition, and Key Sub-Component Applications.

1. By Vehicle Type (Passenger Vehicles vs. Commercial Vehicles)

Passenger Vehicles: This segment is anticipated to remain the fastest-growing and highest-volume segment throughout the forecast period. Rapid global urbanization, rising consumer demand for premium cross-over SUVs, and expanding middle-class disposable income in developing nations are fueling production numbers. Furthermore, passenger cars are subject to the strictest pedestrian protection regulations and crash safety metrics, necessitating highly engineered, energy-absorbing front-end modules.

Light Commercial Vehicles (LCVs) & Heavy Commercial Vehicles: While slower in terms of initial modular adoption compared to passenger vehicles, the commercial segment is steadily adopting front-end modules to lower fleet maintenance costs, improve repairability after low-speed impacts, and reduce overall fleet fuel consumption through mass reduction.

2. By Material Type (Steel, Aluminum, Plastic, Hybrid, and Composites)

Composites and Hybrids: Together, these segments represent the future of front-end carrier design. Plastic-metal hybrids combine the high tensile strength of thin stamped steel sheets with the geometric flexibility and lightness of injection-molded plastics. All-composite structures are leading the premium and electric vehicle sectors due to their rust-proof nature, structural damping qualities, and maximum weight savings.

Steel and Aluminum: Standard steel remains relevant in low-cost, entry-level automotive markets due to low raw material expenses. Aluminum is carve-outs a high-value niche in luxury vehicle segments where premium lightweighting is pursued without migrating entirely to carbon or advanced glass composites.

3. By Key Sub-Component Application Focus

Modern front-end module systems are deeply integrated with latching and closure retention mechanisms to ensure aerodynamic stability and vehicle security. The market segment splits into:

Side Door Latches & Tailgate Latches: Systems integrated into broader platform sourcing strategies.

Hood Latch Assemblies: Directly mounted and calibrated on the central structural beam of the front-end module. The alignment of the hood latch within the FEM is critical for safety, preventing sudden latch failures at highway speeds and ensuring correct energy dissipation during frontal collisions.

Regional Industry Insights: Asia-Pacific Outpaces Global Growth; North America Pivots to Advanced Materials

Asia-Pacific: The Unrivaled Global Production Engine

The Asia-Pacific region stands as the dominant force in the global automotive front-end module market and is poised to maintain its robust growth momentum through 2030. The region's supremacy is fueled by massive manufacturing operations located in China, India, Japan, and South Korea.

China, maintaining its status as the world’s largest single automotive market and producer, is driving the regional market forward through aggressive government incentives and infrastructure investments backing New Energy Vehicles (NEVs). As domestic and international manufacturing joint ventures scale up their EV production lines in China and India, the localized sourcing of integrated front-end modules is expanding exponentially. Rapid urbanization, massive population densities, and rising disposable incomes across Southeast Asian economies further solidify Asia-Pacific as a primary revenue generator for tier-1 front-end system suppliers.

North America: Regulatory Pressures Drive High-Value Material Subscriptions

The North American automotive front-end module market is entering a phase of intense high-value expansion. Historically slower to adopt full structural modular front-ends compared to Western European OEMs, manufacturers across the United States, Canada, and Mexico are now aggressively transitioning to composite and hybrid FEM structures.

This regional shift is primarily enforced by stringent regulatory updates, including corporate average fuel economy (CAFE) standards and evolving pedestrian-protection ratings. To meet these targets without sacrificing the large vehicle footprint preferred by North American consumers—such as full-size pickup trucks and large three-row sport utility vehicles—OEMs are turning to direct long-fiber thermoplastics (D-LFT) and advanced polypropylene compounds. The highly integrated engineering approach allows North American manufacturers to reduce structural weight, simplify vehicle assembly lines, and improve front-impact safety performance simultaneously.

Competitive Landscape

Leading Automotive Front End Module Key Players include:

1. Aisin Seiki Co., Ltd. - Japan

2. Mitsui Mining and Smelting Co., Ltd. - Japan

3. Kiekert AG - Germany

4. Magna International - Canada

5. Prabha Engineering Pvt. Ltd - India

6. Strattec Security Co. - United States

7. U-Shin, Ltd. - Japan

8. Shivani Locks Pvt. Ltd. - India

9. Brose Fahrzeugteile Gmbh & Co. - Germany

10. Inteva Products, LLC. - United States

11. Minda VAST Access Systems Pvt. Ltd. - India

12. DENSO CORPORATION - Japan

13. MAHLE GmbH - Germany

14. Faurecia - France

15. Calsonic Kansei Corporation - Japan

16. HYUNDAI MOBIS - South Korea

17. Plastic Omnium - France

18. SMRPBV - Netherlands

19. SL Corporation - South Korea

20. Valeo - France

21. Montaplast GmbH - Germany

22. Hanon Systems - South Korea

For full access to the comprehensive strategic report, visit:https://www.maximizemarketresearch.com/market-report/automotive-front-end-module-market/16726/

Strategic Implications for Global OEMs: The Decision-Making Framework

For automotive executives, purchasing directors, and design engineers, the decision to implement advanced front-end modules is no longer a matter of simple component sourcing; it is a fundamental strategic choice that dictates the entire capital expenditure (CapEx) profile of a vehicle program.

Making the proper decision requires balancing the slightly higher upfront tooling and development costs of a complex, multi-material composite or hybrid front-end module against the massive, multi-million-dollar savings realized down the line on the factory floor. OEMs must evaluate their manufacturing assets: if an existing assembly plant is undergoing a retooling cycle to accommodate an upcoming EV platform, integrating a modular front-end assembly framework can eliminate substantial factory floor footprint requirements, freeing up high-value space for battery pack installation zones.

Furthermore, long-term profitability in the automotive supply chain will increasingly favor companies that form tight, early-stage engineering alliances. Because a modern front-end module mixes lighting, cooling, structural crash cans, and advanced ADAS sensor arrays into a single physical unit, tier-1 suppliers must be brought into the vehicle design loop years before the first prototype is stamped. OEMs that successfully master this co-development workflow can compress their time-to-market, minimize engineering revisions, and achieve optimal structural performance at minimal cost.

About Maximize Market Research

Maximize Market Research is a multifaceted market research and consulting company with professionals from several industries. Some of the industries we cover include medical devices, pharmaceutical manufacturers, science and engineering, electronic components, industrial equipment, technology and communication, cars and automobiles, chemical products and substances, general merchandise, beverages, personal care, and automated systems. To mention a few, we provide market-verified industry estimations, technical trend analysis, crucial market research, strategic advice, competition analysis, production and demand analysis, and client impact studies.

Contact Maximize Market Research

3rd Floor, Navale IT Park, Phase 2

Pune Bangalore Highway, Narhe,

Pune, Maharashtra 411041, India

sales@maximizemarketresearch.com

+91 96071 95908, +91 9607365656