Market Overview:

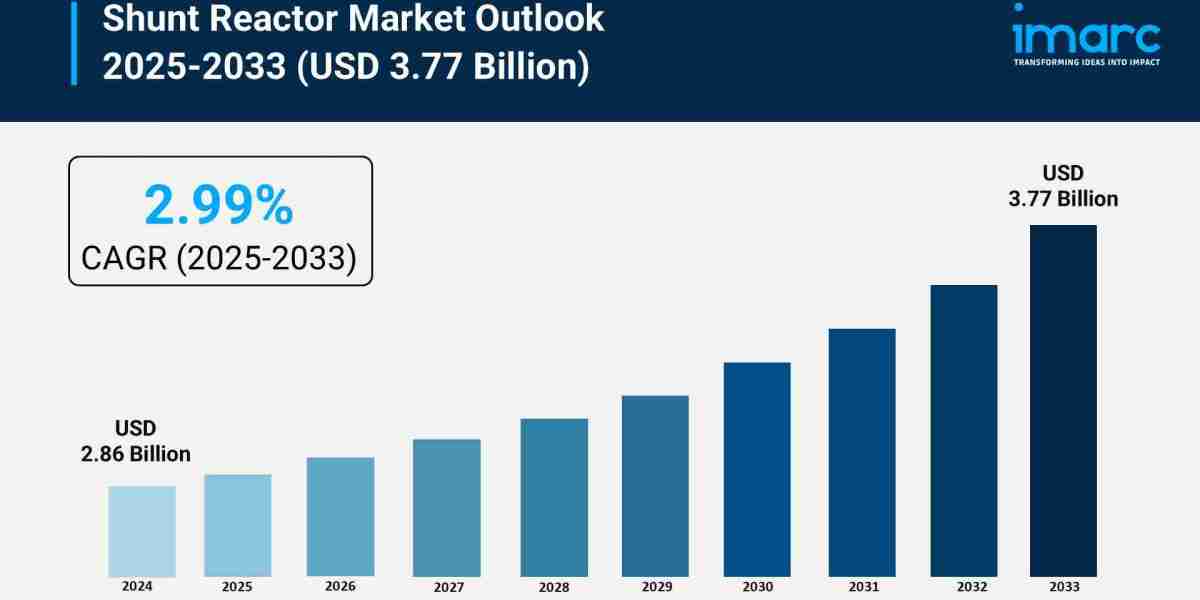

The shunt reactor market is experiencing rapid growth, driven by integration of variable renewable energy sources, global expansion and modernization of transmission networks, and rising global demand for electricity. According to IMARC Group's latest research publication, "Shunt Reactor Market Size, Share, Trends and Forecast by Type, End-User, Application, and Region, 2025-2033", The global shunt reactor market size was valued at USD 2.86 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 3.77 Billion by 2033, exhibiting a CAGR of 2.99% during 2025-2033.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/shunt-reactor-market/requestsample

Our report includes:

- Market Dynamics

- Market Trends and Market Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Growth Factors in the Shunt Reactor Market

- Integration of Variable Renewable Energy Sources

The global drive towards decarbonization and sustainable energy is a primary catalyst for the shunt reactor market. As governments worldwide implement initiatives to boost green energy capacity, the integration of variable sources like solar and wind power into the main electrical grid becomes essential. These sources introduce inherent intermittency and volatility, which can lead to voltage fluctuations and overvoltages in high-voltage transmission lines. Shunt reactors are critical for absorbing the excess capacitive reactive power generated, thereby stabilizing the grid and ensuring reliable power delivery. The Indian Ministry of New and Renewable Energy’s goal to achieve 500 GW of renewable energy capacity, for instance, underscores the massive grid expansion and subsequent demand for reactive power compensation devices in the Asia-Pacific region. Companies like Hitachi Energy are responding with advanced solutions, such as launching specialized shunt reactors for floating offshore wind projects, addressing the unique challenges of deep-water and marine conditions.

- Global Expansion and Modernization of Transmission Networks

The aging power transmission and distribution (T&D) infrastructure in developed economies, coupled with significant expansion in rapidly industrializing regions, necessitates extensive grid modernization efforts. Shunt reactors are essential components in these projects, particularly in high-voltage and ultra-high-voltage (UHV) transmission lines that span long distances. The United States, for example, is making robust investments in upgrading its grid systems to improve resilience and reliability. Concurrently, countries across the Asia-Pacific region, driven by rapid urbanization and industrial growth, are heavily investing in new transmission corridors and substations to connect growing power generation capacity to consumers. This two-pronged approach—upgrading old systems and building new ones—significantly increases the deployment of both fixed and variable shunt reactors to maintain optimal voltage levels and reduce transmission losses across the expanding and more complex network.

- Rising Global Demand for Electricity

The continuous increase in global electricity consumption, fueled by population growth, urbanization, and the electrification of various sectors, is a fundamental factor driving the demand for all power system components, including shunt reactors. This growing energy appetite puts immense pressure on power grids to operate efficiently and reliably. The International Energy Agency projects global electricity consumption to grow annually, highlighting the persistent need for stable power transmission. The proliferation of electric vehicles (EVs) is a notable subset of this demand, as the need for extensive charging networks and the associated spikes in power draw require enhanced voltage control across the distribution grid. Consequently, utilities are compelled to invest in reactive power compensation technologies to mitigate potential voltage issues, ensuring a continuous and stable power supply to both residential and increasingly energy-intensive industrial consumers like data centers.

Key Trends in the Shunt Reactor Market

- Shift Towards Variable Shunt Reactors (VSRs)

There is a pronounced industry trend toward adopting Variable Shunt Reactors (VSRs) over traditional fixed shunt reactors, driven by the increasing need for dynamic and precise voltage control. VSRs can continuously and automatically adjust the amount of reactive power they absorb in real time, offering greater flexibility to adapt to the highly fluctuating conditions characteristic of modern grids that incorporate substantial renewable energy. This is particularly crucial on long transmission lines where load and generation patterns change frequently. The flexibility of VSRs supports grid operators in meeting stringent reliability and power quality standards. For instance, companies are developing and launching high-voltage VSRs, such as one model operating at 500 kV, specifically designed to better integrate high-capacity, intermittent renewable resources like large-scale wind and solar farms by maintaining stable voltage levels under diverse operating scenarios.

- Growing Adoption of Air-Core Dry-Type Reactors

An emerging trend is the increasing preference for Air-Core Dry-Type Reactors over conventional oil-immersed designs, especially in lower to medium-voltage applications and in environmentally sensitive locations. These reactors use air as the insulating medium instead of mineral oil, eliminating the risk of oil leakage, reducing fire hazards, and minimizing environmental impact. While oil-immersed units continue to dominate in ultra-high-voltage applications above 400 kV due to superior insulation, dry-type technology is rapidly gaining traction for projects with strict environmental and safety mandates. Their compact footprint and reduced maintenance requirements also make them highly suitable for installation in space-constrained environments, such as urban substations and some specialized industrial settings. Manufacturers are investing in R&D to expand the voltage rating and performance capabilities of these environmentally neutral solutions.

- Digitalization and Integration with Smart Grid Technology

The market is moving toward the Digitalization and Integration of Shunt Reactors with broader smart grid technologies, enhancing their monitoring, control, and efficiency. This involves embedding advanced sensors and digital communication capabilities—often referred to as 'smart reactors' or 'IoT-enabled' equipment—to provide real-time operational data. This data enables utilities to perform predictive maintenance, optimize reactor settings remotely, and improve overall system reliability. For example, the incorporation of advanced monitoring and diagnostic systems allows grid operators to track parameters like temperature, vibration, and winding integrity continuously. This digital integration is a key component of grid automation efforts globally, supporting the transition from reactive maintenance schedules to proactive, condition-based interventions, which ultimately lowers operational costs and extends the service life of these critical high-value assets.

Leading Companies Operating in the Global Shunt Reactor Industry:

- ABB Ltd.

- General Electric (GE) Company

- Siemens AG

- Nissin Electric Co. Ltd.

- PrJSC Zaporozhtransformator

- CG Power and Industrial Solutions Limited

- Alstom SA

- Hyundai Heavy Industries Co., Ltd.

- Mitsubishi Electric Corporation

- Hitachi, Ltd.

- Toshiba Corporation

- Hilkar Electric Limited

- Fuji Electric Co., Ltd.

- TBEA Co., Ltd.

- Trench Group

Shunt Reactor Market Report Segmentation:

By Type:

- Oil-Immersed

- Air-Core

- Others

Oil-immersed reactors dominate due to superior cooling capabilities and higher power ratings for transmission applications.

By Application:

- Transmission Systems

- Distribution Systems

- Others

Transmission systems represent the largest segment driven by high-voltage grid expansion and renewable energy integration needs.

By Voltage Rating:

- Low Voltage

- Medium Voltage

- High Voltage

- Extra High Voltage

High voltage segment holds majority share due to long-distance transmission requirements and grid interconnection projects.

By Installation:

- Outdoor

- Indoor

Outdoor installations account for larger share due to space availability and cost considerations in transmission substations.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia Pacific held over 40% market share in 2024, driven by industrialization and energy infrastructure growth.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302